前面文章中,详细介绍了用批量梯度下降法(BGD),求解线性回归问题的过程。本文再另外介绍两种:随机梯度下降(SGD)和小批量梯度下降(MBGD),并使用图形的方式,对三种方法做一个横向对比。

import numpy as np

X = np.linspace(-1, 1, 100)

y = 5 * X # 精简目标函数

def func(x, a):

return a * x

# learning rate

lr = 0.05

批量梯度下降(Batch Gradient Descent BGD)

批量梯度下降,会遍历全部数据集算一次损失函数,然后算函数对各个参数的梯度,更新梯度。这种方法每更新一次参数,都要把数据集里的所有样本计算一遍,计算量大,计算速度慢。

a_bgd = 0

a_bgd_list = []

for step in range(200):

a_sum = 0

for idx, x in enumerate(X):

a_sum += (func(x, a_bgd) - y[idx]) * x

a_bgd -= lr * a_sum / len(X)

a_bgd_list.append(a_bgd)

随机梯度下降(Stochastic Gradient Descent SGD)

随机梯度下降,是每次从训练集中随机选择一个样本,计算其对应的损失和梯度,进行参数更新,反复迭代。

这种方式在数据规模比较大时可以减少计算复杂度,从概率意义上来说的单个样本的梯度,是对整个数据集合梯度的无偏估计,但是它存在着一定的不确定性,因此收敛速率比批梯度下降得更慢。

a_sgd = 0

a_sgd_list = []

for step in range(200):

idx = np.random.randint(len(X))

x = X[idx]

a_sum = (func(x, a_sgd) - y[idx]) * x

a_sgd -= lr * a_sum

a_sgd_list.append(a_sgd)

小批量梯度下降(Mini-batch Gradient Descent)

为了克服上面两种方法的缺点,采用的一种折中手段:将数据分为若干批次,按批次更新参数,每一批次中的一组数据共同决定了本次梯度的方向,下降起来就不容易跑偏,减少了随机性,另一方面,因为批的样本数比整个数据集少了很多,计算量也不是很大。

a_mbgd = 0

a_mbgd_list = []

for step in range(200):

a_sum = 0

idx = np.random.randint(len(X) - 10)

for i in range(10):

x = X[idx + i]

a_sum += (func(x, a_mbgd) - y[idx + i]) * x

a_mbgd -= lr * a_sum

a_mbgd_list.append(a_mbgd)

对比和总结

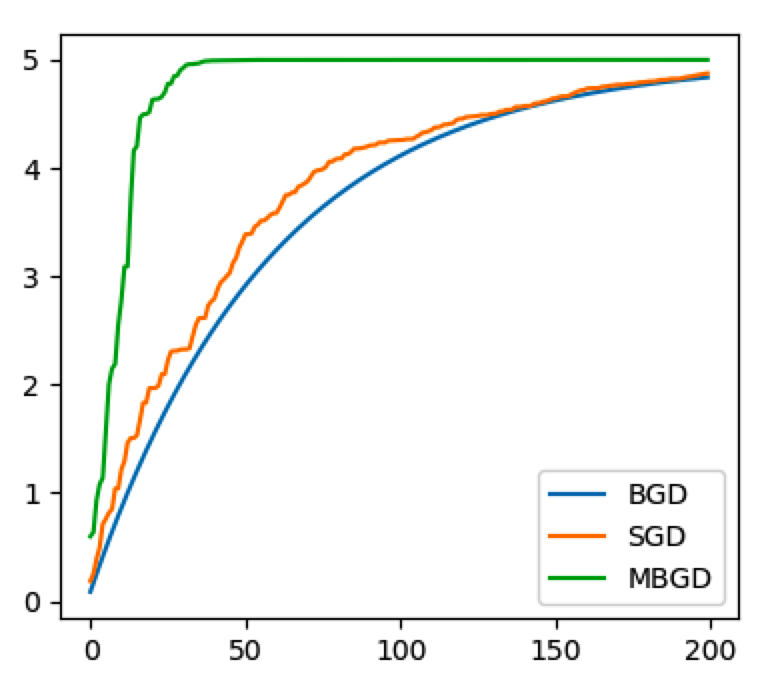

from matplotlib import pyplot as plt plt.plot(range(200), a_bgd_list, label='BGD') plt.plot(range(200), a_sgd_list, label='SGD') plt.plot(range(200), a_mbgd_list, label='MBGD') plt.legend() plt.show()

三种方法比较

1) SGD和BGD的迭代次数,要大于MBGD;

2) BGD一定能够得到一个局部最优解,SGD由于随机性的存在可能导致最终结果比BGD的差;

3) SGD有可能跳出某些小的局部最优解,所以一般情况下不会比BGD坏。

在实际项目中,一般优先使用SGD。

本文为 陈华 原创,欢迎转载,但请注明出处:http://www.ichenhua.cn/read/253

- 上一篇:

- 手写AI算法之梯度下降法求解线性回归

- 下一篇:

- 时间复杂度和空间复杂度